At a time when every financial decision is so important, many small and medium-sized businesses (SMBs) can take at least some comfort in knowing they have a variety of borrowing tools available to them if they need to.

Today's entrepreneurs can choose from credit cards that earn them rewards. Shop loan. Bank loans; buy now, pay later (BNPL) products. lines of credit, etc.

However, according toSMB Borrowing Trends: Trends, Tools, and Decision Factors”, PYMNTS Intelligence and us bank Small businesses need to consider a variety of factors before choosing a borrowing tool that makes sense for them.

Company size, revenue levels, leadership goals, cash flow, and expenses all need to be considered. Small business owners also need to consider how flexible and accessible they want their borrowing options to be.

Differences in priorities will determine the final decision. For example, 73% of all small businesses surveyed use revolving credit, but low-revenue small businesses (less than $1 million in annual revenue) are more likely than high-profit small businesses (more than $10 million in annual revenue). (Companies) use borrowing tools less frequently than other companies. ). In fact, low-profit SMEs tend to prioritize immediate working capital needs and financial stability relative to high-profit SMEs, which are more focused on business expansion and growth goals.

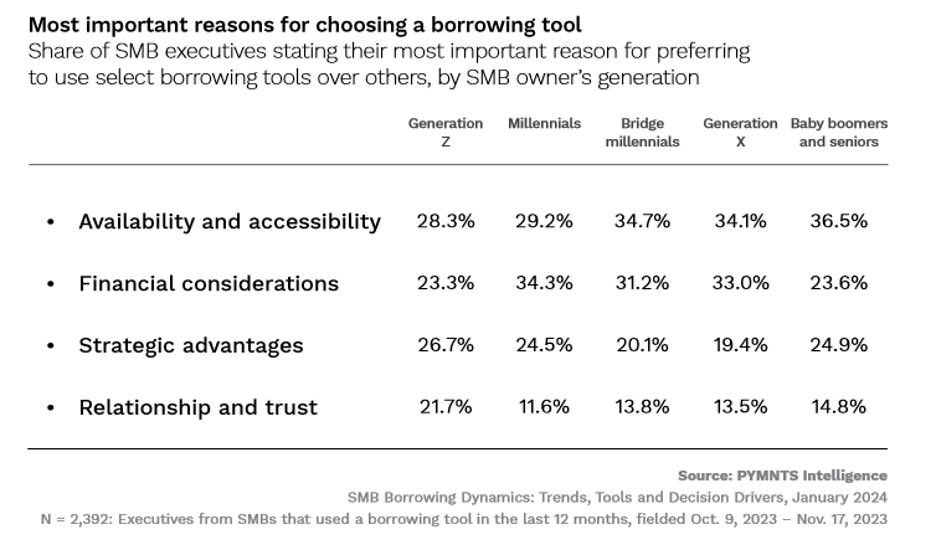

75% of SMEs cite the availability and accessibility of finance as a key concern when evaluating and using borrowing tools, making flexible financing solutions fundamental and essential for SMEs. important needs are highlighted. Meanwhile, 71% prioritize financial considerations such as favorable payment terms (33%), lower borrowing costs (26%) and the potential for improved credit scores (23%). The importance of relationships and trust is less important, with only 14% of small and medium-sized enterprises citing these as their top priority.

SMEs' preferences in choosing borrowing tools also appear to be shaped by generational perspectives.

For example, as the figure above shows, 37% of small businesses owned by baby boomers and older adults emphasize the importance of credit availability and accessibility, while 37% of small businesses owned by baby boomers and older adults emphasize the importance of credit availability and accessibility. Generation-owned businesses were less influenced by these characteristics, at 28% and 29%. Each.

However, fewer small and medium-sized businesses are owned by Millennials (34%), Bridge Millennials (31%), and Gen For businesses, financial considerations are more important.

Interestingly, although there is only a few years difference between Millennials and Gen Z small business owners, younger entrepreneurs are more likely to value and trust their relationships with financial institutions by 22% of respondents say these are key factors, nearly double the 12% share among Millennials, the data shows. owners.

This data provides insight for lenders looking to partner with small and medium-sized businesses. This means that lenders need to take into account what preferences are attractive to business owners before recommending a product.