The ABS defines net worth as the value of all assets owned by a household minus its liabilities, which includes the home and its contents, land, vehicles, businesses and financial assets such as bank accounts, shares and pension accounts. It found that primary residences accounted for 40% of household net worth in 2019-20, followed by pensions at 18%.

The average net worth of the wealthiest 20 percent of households was $3.27 million.

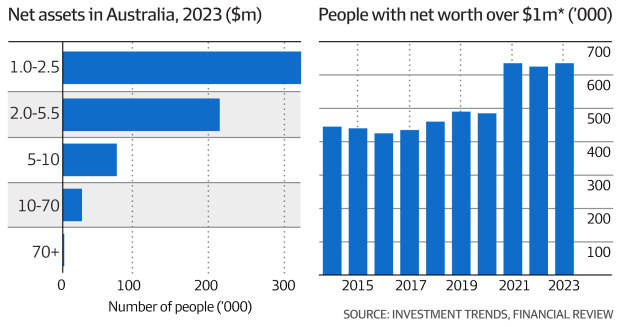

There are 635,000 'high net worth' people in Australia, making up about 2.5% of the total population.

A report by global real estate consultancy Knight Frank says an Australian needs a net worth of at least US$1 million ($1.5 million) to be considered wealthy — a calculation that also includes a primary residence — but to be in the top 1% of Australians, Knight Frank says you need a net worth of US$4.67 million.

Financial research firm Investment Trends also put the numbers to work to determine who is wealthy in Australia today, defining the ultra-wealthy in Australia as people with a net worth of more than $1 million, excluding the value of their home, their business (if they own one), and their superannuation (but including any self-managed super fund assets).

According to the 2023 High Net Worth Investors Report, by this measure, there are 635,000 high net worth individuals in Australia, making up about 2.5% of the total population. According to the company's research, people with assets of more than $2.5 million are in the top 1.5%, while those with assets of more than $5 million are in the top 0.5%.

Eileen Giamascia, head of research at Investment Trends, said there will be 150,000 new ultra-wealthy individuals between 2020 and 2021. Rhett Wyman

Investment Trends breaks down the wealth measure further, dividing wealth into three categories: those with a net worth between $1 million and $2.5 million are Emerging Wealthy, those with a net worth between $2.5 million and $10 million are Established Wealthy, and those with over $10 million are Ultra-Wealthy (UHNW).

Dr Eileen Giamascia, head of research at Investment Trends, said after a small drop of 10,000 in 2022, the number of Australians classed as high net worth in 2023 was the same as in 2021. But the real movement came between 2020 and 2021, with 150,000 new ultra-high net worth individuals being created, the majority of whom joined the emerging wealthy category. “We think this is due to a kind of bubble of everything we've seen during the pandemic, which is why stocks have skyrocketed, why property prices have skyrocketed,” she said.

Investment Trends notes that within the ultra-wealthy bracket, there's been some movement between subgroups, with the wealthy getting even wealthier. Between 2022 and 2023, an additional 45,000 people were added to the wealthy bracket, which Giamascia attributes to the strong performance of stocks and real estate, the assets that this group is most exposed to.

Indicators of wealth

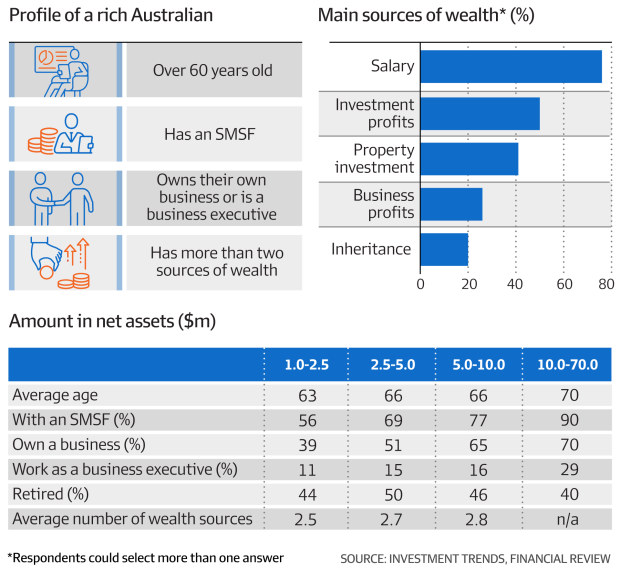

So what do the wealthy have in common? According to a survey by Investment Trends, more than half of all high net worth individuals have an SMSF, with that figure rising to 90% for Australia's ultra-high net worth individuals.

The average age of Australia's overall HNWIs is over 60, and as the HNWI ranks, they get older. The average age of the Emerging HNWIs is 63, the average age of the Established HNWIs is 66, and the average age of the Ultra-HNWIs is 70.

They most commonly work as business executives, engineers, doctors, accountants, IT professionals and financial advisors, but more than half of the established and ultra-wealthy own their own businesses. In terms of source of wealth, around three-quarters derive their primary source from a salary, but at the bottom end of the wealth ladder this figure is much higher: over 80% of the emerging wealthy derive their wealth primarily from a salary, compared to just 55% of the ultra-wealthy.

On average, all wealthy people have at least two sources of income, and the wealthier they are, the more sources they have. After salary, the most common ways that wealthy people acquire wealth are investment income (50%), real estate investments (41%), business income (26%), and inheritances (20%). In terms of how they invest, Giamacia said that a typical portfolio of a wealthy person tends to be “about one-third in stocks, one-third in real estate, and the remaining third diversified into other assets such as cash, fixed deposits, and private equity.”

How to join the club

We're not there yet, but if you want to join the ranks of the wealthy, you need to be in it for the long haul, says Ben Smythe, principal adviser and partner at Minchin Moore. His wealthy clients “are not looking for quick fixes or get rich quick schemes,” he says.

“They've built their wealth methodically, slowly and methodically and aren't looking for shortcuts or get-rich-quick schemes,” he says, “which I think is where a lot of people get caught up and fall into, trying to get rich quick.”

According to him, the wealthy favor a long-term strategy of preserving quality assets by buying and holding rather than buying and selling assets, and they place emphasis on building diversified portfolios and managing liabilities properly, distinguishing between good and bad debt: “Good debt is related to investment assets and has deductible interest, while bad debt is personal equity debt that cannot be deducted. Over-reliance on bad debt makes it very hard to build wealth.”

He says that while many wealthy people may have an SMSF, it's not a panacea: “An SMSF is just a structure and it's not going to miraculously give you double-digit returns. You need a well-thought-out plan based on a long-term strategy before that happens. Successful people take the time to hire an adviser or become financially literate themselves.”

As for displays of wealth and ostentatious consumption, Smythe says these tend to be more common among people who inherited wealth. “The first generation, who made their wealth, especially in small businesses, are incredibly frugal and very diligent in terms of knowing where their money is going. The second and third generations probably have a different mindset.”