believes it can drive business growth")

Even when a company is losing money, shareholders can make money by buying a good company at the right price. For example, Salesforce.com, the software-as-a-service company, lost money for years while its recurring revenues were growing, but if you held its shares since 2005 you would certainly have made a lot of money. That said, only a fool would ignore the risk that a loss-making company could burn through its cash too quickly.

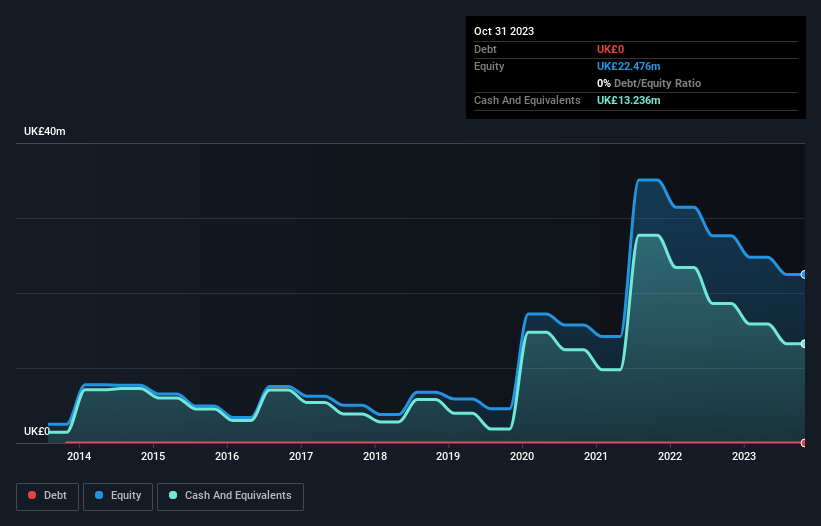

That's what you should do Ilika Are (LON:IKA) shareholders worried about the company's cash burn? In this report, we'll look at the company's negative free cash flow (hereafter referred to as “cash burn”) for the year. Let's start by looking at the cash of the business compared to the company's cash burn.

Check out our latest analysis for Ilika

How long is Ilika's cash runway?

Cash runway is defined as the length of time it would take a company to run out of funds if it kept spending at its current cash burn rate. When Ilika last reported its balance sheet for October 2023, in January 2024, it had zero debt and cash of GBP13m. Importantly, its cash burn over the trailing 12 months was GBP5.5m, which means it had a cash runway of around 2.4 years from October 2023. This is plenty, giving the company several years to operate. Below you can see how its cash holdings have changed over time.

How has Ilika's cash burn changed over time?

Ilika made revenue of £1.8 million in the past 12 months. operating Revenues for that period were just UK£40k. Because the company is growing from a low base, we don't think there's enough operating revenue to interpret too much from the revenue growth rate, which is why we'll focus on cash burn today. While it does little to paint a picture of imminent growth, the fact that it has reduced its cash burn by 38% over the past year suggests some prudence. It's always worth studying the past, but it's the future that matters most, which is why it makes a lot of sense to take a look at analyst forecasts for the company.

How easily can Ilika raise funds?

Despite reducing its cash burn recently, shareholders should consider how easy it will be for Ilika to raise more cash in the future. Companies can raise capital through either debt or equity. One of the main advantages that publicly traded companies have is that they can sell shares to investors to raise cash to fund growth. Looking at a company's cash burn relative to its market capitalization can give us an idea of how much dilution shareholders would face if the company needed to raise enough cash to cover its cash burn over the next year.

With a market cap of UK£46m, Ilika's cash burn of UK£5.5m equates to roughly 12% of its market cap. As a result, we expect the company will be able to raise further capital for growth without much issue, albeit at the cost of dilution.

Are you worried about Ilika's cash burn?

As you may have already guessed, we are relatively comfortable with how Ilika is using its cash. For example, we think the company's cash runway indicates that it is on a good track. Its cash burn relative to its market cap is not as good, but it's still pretty encouraging. Given all the factors we've discussed in this article, we're not too worried about the company's cash burn, but we do think shareholders should keep an eye on how it plays out. After examining the risks in more detail, we find that: 4 warning signs for Ilika Things you should know before investing.

of course, You may find a great investment by looking elsewhere. Take a look at this free A list of companies with significant insider holdings and a list of growth stocks predicted by analysts

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.